What is GSTR-2

What is GSTR-2?

2. Why is GSTR-2 important?

3. What is buyer-seller reconciliation?

4. When is GSTR-2 due?

- Businesses with annual turnover up to 1.5 crores will submit quarterly returns. Taxes will be paid quarterly.

- Due dates of Aug & Sep will be declared later.

- Switch over to quarterly will happen from Oct-Dec 2017 cycle

5. What happens if GSTR-2 is not filed?

6. What happens if GSTR-2 is filed late?

7. Who should file GSTR-2?

- Input Service Distributors

- Composition Dealers

- Non-resident taxable person

- Persons liable to collect TCS

- Persons liable to deduct TDS

- Suppliers of online information and database access or retrieval services (OIDAR), who have to pay tax themselves (as per Section 14 of the IGST Act)

8. How to revise GSTR 2?

9. What is GSTR-2A?

10. How to file GSTR 2 on ClearTax GST software?

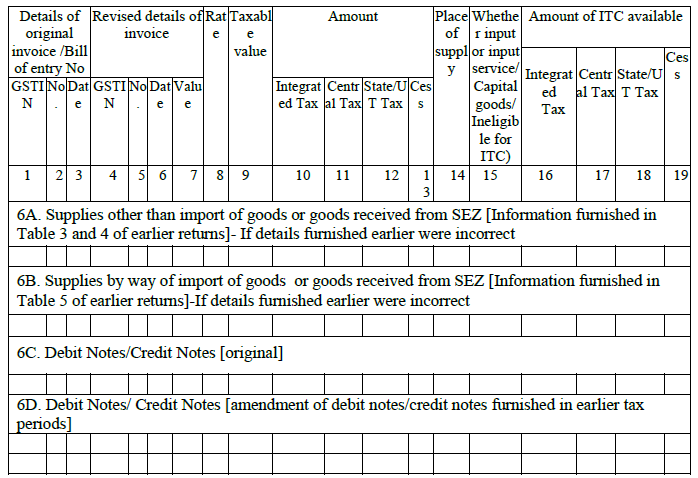

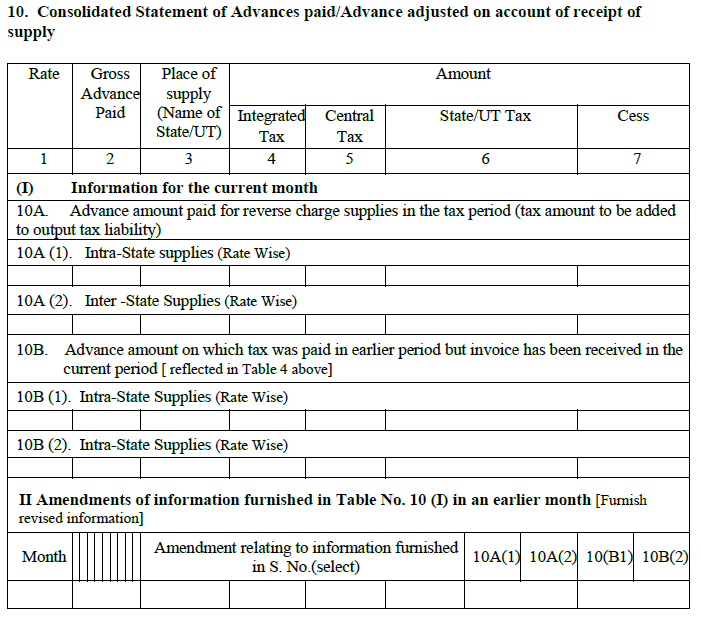

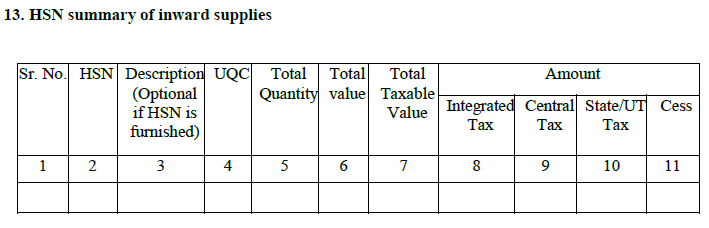

11. Details to be provided in GSTR-2

- 5B. Received from SEZ: Inputs or capital goods received from sellers in a SEZ will be reported here.

- This part will cover the advance amount paid for reverse charge supplies in the current month.

- It will also include the advances paid in earlier months against which invoices have been received in current month.

- The purchases will be broken up into inter-state and intra-state.

d. Amount in terms of rule 43(1)(h)– This is similar to above except that it concerns capital goods.

Comments

Post a Comment